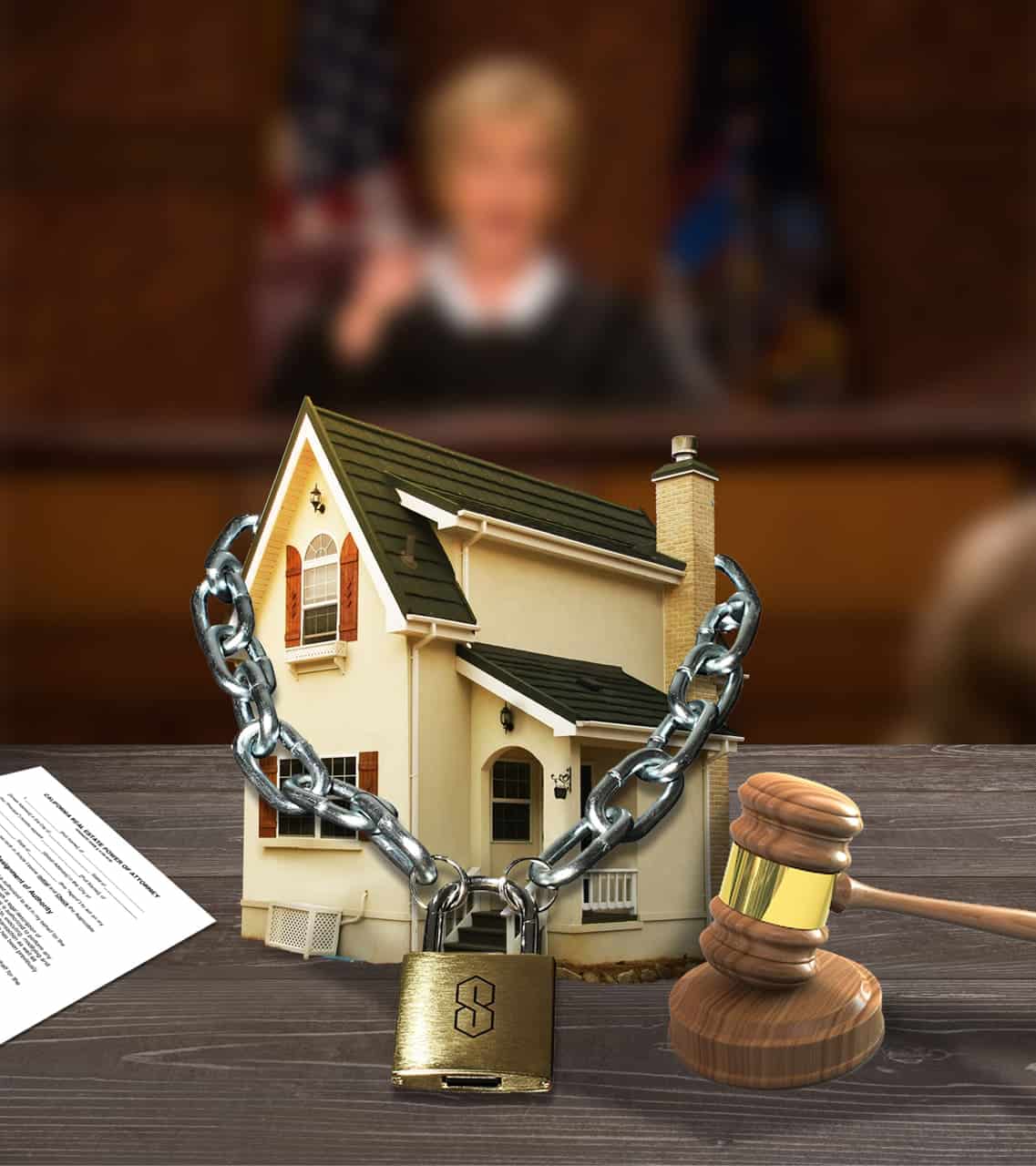

Credit judgments and liens on the title can be extremely stressful situations. There is a bad patch for every homeowner. A financial emergency, a sudden medical burden, or even unexpected unemployment, amongst other circumstances, can cripple your ability to pay off your mortgage. This not only creates complications with liens on the title, but it also hurts your credit score and your financial security.

If you are no longer able to repay your financial obligation towards your lender, it will undoubtedly lead towards negative judgment and, eventually, being slapped with a lien on your property title. Carrying debt on the home, be it for a business loan, a home mortgage, or a new car, can be increasingly challenging. Having liens on title lead to the most stressful and challenging financial cycles for homeowners.

There are various kinds of liens on the title, depending on the creditor and the type of debt that you owe. You may have a lien on the title by the Internal Revenue Services, which means that you owe a debt of federal income taxes. If your property taxes are not paid regularly, the county can impose a tax lien. If you fail to repay your debts to a lender, a general judgment lien will be imposed.

In such circumstances, you can sell off or refinance your home to pay off the lender and eliminate the debt on the home. However, if your lender decides not to allocate you sufficient time to sell off or refinance your property, he/she can execute the lien on the title by requesting the court for permission to sell off your property to recover the debt. This basically indicates that if there is sufficient equity in the property, the judgment creditor will have the right to force the sale of the property to collect upon the judgments.

Liens on title can be extremely hurtful for a homeowner, but only in the instance when you start falling back on your mortgage payment. You will either be forced to sell off your property as you will be sharing the ownership of your property with the lender to whom you owe money. A lien on title basically indicates that your debt has been unfilled, and legal judgments will come into play. A lien on the title does not indicate that your property has been transferred to another owner, but it is indeed a step towards that direction, should your lender choose to take that route.

In such a situation, your ideal choice is to avoid the worst-case scenario of your property being seized and sold off without your consent. This usually is the case when you are unable to pay off your property taxes. You can free yourself of the burden of carrying debt on your home by selling off your property and using that money to pay off your debts, and starting afresh in the real estate market.

It may seem daunting and challenging, and we advise you to get in touch with our team to devise a comprehensive strategy.

When Would You Like To Sell Your House?

Are you a property owner?

Reason To Sell